Would seem to be an improvement -

The March numbers are in, and as noted by the FH they seem to be a bit better. But interesting to relate that the FH has taken to tempering their feedback of late, stating essentially that although this is an improvement, don't read too much into it.

But there are a few other indicators out there that might shed a wee bit of sunshine. Per some reports, the total number of retail store closures in North America has been down this first quarter. And that is a potentially positive development as well. But these same outlets also report that the number of NEW North American retail stores is also down.

Obviously, it is in the best interest of everyone involved if the industry rebounds. But this has been a beat-down of nearly epic proportions for brands, distributors, retailers and yes, even customers. A beat-down the likes of which we haven't seen since the "Quartz Crisis". And while there were real lessons learned from that paradigm shift, it remains to be seen if this current paradigm shift will illicit the same level of introspection at the higher echelons.

And while the rate of decline is slowing, it does not necessarily mean that we are in blue sky territory. What it most likely means is that the rubber has finally hit the road and at least some of the brands, distributors and retail store owners are starting to realize that things are most likely not going to rebound back to the level that they were. Production, sales forecasts and pricing might finally be getting closer scrutiny. The perceived need to carry such large staffs both in Switzerland and in the "outposts" might be getting a second look as well.

And we have anecdotal evidence that clearly shows that brands and those dependent upon those brands are starting to change their attitudes and approaches. Some for sound business reasons, some just out of panic:

BaselWorld - will be reduced by 2 full days with participation fees (reportedly) to be reduced to reflect this change. With attendance down again for retailers and journalists, this was most likely a very cold cup of espresso for the BaselWorld organizers to swallow, but the numbers just don't lie. It was a bold decision to take, and one that I agree with.

SIHH - 'nuff said.

Brand Managers - several found themselves let go just before and just after BaselWorld. This is not exactly a new development, but the level and depth of these cuts was a little more marked this year. So brands are going to be REALLY looking at who is performing and who isn't. Tough love time.

The "Soft Grey" Market - well known brands are clearly not selling at the level that the could or should, and growing portions of their stocks are being dumped into group buy sites. Merchandise has to be moved, and this seems to be the most acceptable of a lot of really unacceptable solutions.

And then, as always, there will be holdouts:

The Brand Boutique - for a few independent brands, there is still a monumental disconnect on the realities of their given situations and they continue to insist on dropping more and more money into a boutique that can never really pay for itself. For a group brand? No big deal, it is a marketing expense. For an independent brand? It is an ego stroke and a fairly clear disregard for reality. And it also reflects the Sunk Cost Fallacy (please refer back to the Sunk Cost Trap - http://www.tempusfugit.watch/2017/04/the-sunk-cost-trap.html for further examples) that is at work at the highest levels of some of these brands. When you have sunk as much money as some independents have into these boutiques, it becomes harder and harder to walk away.

Now contrary to the frantic assertions of a certain watch industry writer, I am not the Antichrist. I truly take no satisfaction in seeing the industry suffer. But I also believe that just because you trim a donkey's ears, that doesn't suddenly give you a Shetland Pony.

Some of the industry is moving to adapt, and some particularly sharp operators have been a few steps ahead and have done okay even during this downturn. The real challenge now is for the remaining denizens of planet "Watch" to decide if they are ready to adapt or not.

Because while a reduced loss is better than an increased one, it is still a loss.

|

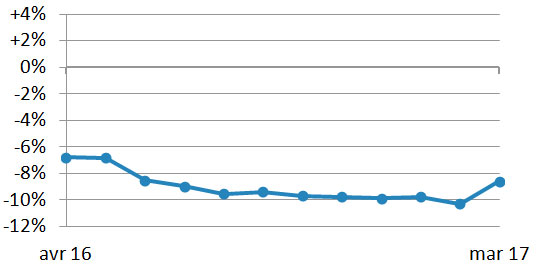

| Courtesy of the FH |

The March numbers are in, and as noted by the FH they seem to be a bit better. But interesting to relate that the FH has taken to tempering their feedback of late, stating essentially that although this is an improvement, don't read too much into it.

But there are a few other indicators out there that might shed a wee bit of sunshine. Per some reports, the total number of retail store closures in North America has been down this first quarter. And that is a potentially positive development as well. But these same outlets also report that the number of NEW North American retail stores is also down.

Obviously, it is in the best interest of everyone involved if the industry rebounds. But this has been a beat-down of nearly epic proportions for brands, distributors, retailers and yes, even customers. A beat-down the likes of which we haven't seen since the "Quartz Crisis". And while there were real lessons learned from that paradigm shift, it remains to be seen if this current paradigm shift will illicit the same level of introspection at the higher echelons.

And while the rate of decline is slowing, it does not necessarily mean that we are in blue sky territory. What it most likely means is that the rubber has finally hit the road and at least some of the brands, distributors and retail store owners are starting to realize that things are most likely not going to rebound back to the level that they were. Production, sales forecasts and pricing might finally be getting closer scrutiny. The perceived need to carry such large staffs both in Switzerland and in the "outposts" might be getting a second look as well.

And we have anecdotal evidence that clearly shows that brands and those dependent upon those brands are starting to change their attitudes and approaches. Some for sound business reasons, some just out of panic:

BaselWorld - will be reduced by 2 full days with participation fees (reportedly) to be reduced to reflect this change. With attendance down again for retailers and journalists, this was most likely a very cold cup of espresso for the BaselWorld organizers to swallow, but the numbers just don't lie. It was a bold decision to take, and one that I agree with.

SIHH - 'nuff said.

Brand Managers - several found themselves let go just before and just after BaselWorld. This is not exactly a new development, but the level and depth of these cuts was a little more marked this year. So brands are going to be REALLY looking at who is performing and who isn't. Tough love time.

The "Soft Grey" Market - well known brands are clearly not selling at the level that the could or should, and growing portions of their stocks are being dumped into group buy sites. Merchandise has to be moved, and this seems to be the most acceptable of a lot of really unacceptable solutions.

And then, as always, there will be holdouts:

The Brand Boutique - for a few independent brands, there is still a monumental disconnect on the realities of their given situations and they continue to insist on dropping more and more money into a boutique that can never really pay for itself. For a group brand? No big deal, it is a marketing expense. For an independent brand? It is an ego stroke and a fairly clear disregard for reality. And it also reflects the Sunk Cost Fallacy (please refer back to the Sunk Cost Trap - http://www.tempusfugit.watch/2017/04/the-sunk-cost-trap.html for further examples) that is at work at the highest levels of some of these brands. When you have sunk as much money as some independents have into these boutiques, it becomes harder and harder to walk away.

Now contrary to the frantic assertions of a certain watch industry writer, I am not the Antichrist. I truly take no satisfaction in seeing the industry suffer. But I also believe that just because you trim a donkey's ears, that doesn't suddenly give you a Shetland Pony.

Some of the industry is moving to adapt, and some particularly sharp operators have been a few steps ahead and have done okay even during this downturn. The real challenge now is for the remaining denizens of planet "Watch" to decide if they are ready to adapt or not.

Because while a reduced loss is better than an increased one, it is still a loss.

No comments:

Post a Comment